New York State income tax is a crucial financial obligation for residents and businesses operating within the state. Understanding the intricacies of this tax system is essential for effective financial planning and compliance with state regulations. Whether you're a new resident, a business owner, or simply looking to improve your knowledge of New York's tax structure, this guide will provide you with the necessary insights to navigate the process successfully.

New York State income tax has always been a topic of interest for taxpayers due to its complexity and the various factors that influence tax liabilities. The state's progressive tax system ensures that individuals and corporations pay taxes according to their income levels, promoting fairness in taxation. As a result, staying informed about the latest tax laws and regulations is vital for ensuring compliance and avoiding penalties.

This article will delve into the details of New York State income tax, including the latest rates, filing requirements, deductions, and credits available to taxpayers. By the end of this guide, you'll have a clear understanding of how the system works and how to optimize your tax situation to maximize savings while fulfilling your legal obligations.

Read also:Gregory Abbott Now The Journey Of A Musical Legend

Table of Contents

- Introduction to New York State Income Tax

- New York State Income Tax Rates

- Filing Status and Requirements

- Deductions and Credits

- Tax Filing Deadlines

- Penalties for Late Filing

- Business Income Tax in New York

- Tax Obligations for Non-Residents

- Resources for Taxpayers

- Conclusion and Call to Action

Introduction to New York State Income Tax

New York State income tax is levied on individuals, trusts, estates, and corporations earning income within the state. The tax system is designed to generate revenue for state operations while ensuring that taxpayers contribute equitably based on their financial capabilities. Understanding the basics of this tax structure is crucial for both residents and businesses operating in New York.

The New York State Department of Taxation and Finance oversees the administration and enforcement of income tax laws. Taxpayers must file annual returns to report their income and pay the appropriate amount of tax owed. Additionally, the state offers various deductions and credits to help reduce tax liabilities for eligible individuals and businesses.

Key Features of New York State Income Tax

- Progressive tax rates based on income levels

- Special provisions for low-income taxpayers

- Deductions and credits for education, healthcare, and other expenses

- Joint filing options for married couples

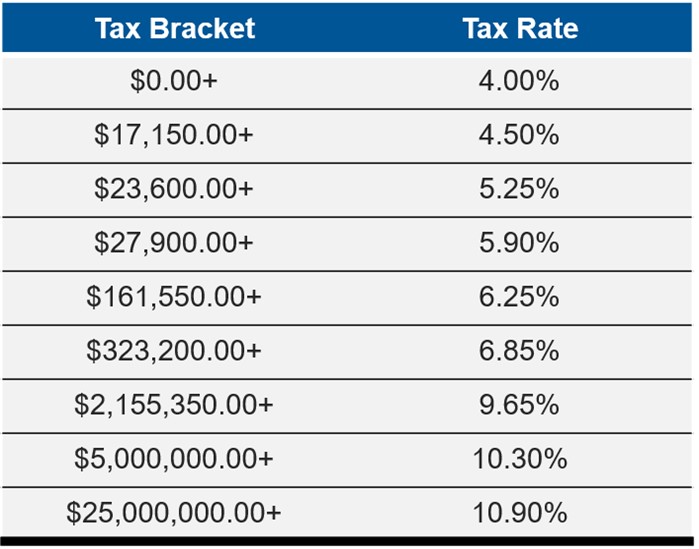

New York State Income Tax Rates

The tax rates in New York State are progressive, meaning that higher income levels are taxed at higher rates. For the 2023 tax year, the state applies the following tax brackets:

2023 Tax Brackets for Individuals

- 4% on the first $8,600 of taxable income

- 4.5% on income between $8,601 and $11,700

- 5.25% on income between $11,701 and $13,900

- 5.97% on income between $13,901 and $21,800

- 6.09% on income between $21,801 and $81,100

- 6.23% on income over $81,100

These rates are subject to change annually, so it's important to consult the latest guidelines from the New York State Department of Taxation and Finance for the most accurate information.

Filing Status and Requirements

Taxpayers in New York State must determine their filing status to ensure accurate tax reporting. The most common filing statuses include single, married filing jointly, married filing separately, and head of household. Each status has specific requirements and benefits that can affect tax liabilities and credits.

Eligibility for Filing Statuses

- Single: Applicable to individuals who are unmarried or legally separated as of December 31.

- Married Filing Jointly: Allows couples to file a single return and combine their incomes.

- Married Filing Separately: Enables spouses to file separate returns, which may be beneficial in certain circumstances.

- Head of Household: Available to unmarried individuals who maintain a home for a qualifying dependent.

Choosing the correct filing status can significantly impact your tax obligations, so it's important to review your situation carefully before filing.

Read also:New York State Income Tax A Comprehensive Guide For Residents And Taxpayers

Deductions and Credits

New York State offers a variety of deductions and credits to help taxpayers reduce their taxable income and lower their overall tax burden. These benefits are designed to support specific groups, such as low-income families, students, and small business owners.

Popular Deductions and Credits

- Standard Deduction: Automatically applied to reduce taxable income for most taxpayers.

- Itemized Deductions: Allow taxpayers to deduct specific expenses, such as mortgage interest and charitable contributions.

- Child Tax Credit: Provides a credit for taxpayers with qualifying dependents.

- Earned Income Tax Credit (EITC): Offers a refundable credit for low- to moderate-income taxpayers.

Consulting with a tax professional or using tax preparation software can help ensure that you take full advantage of all available deductions and credits.

Tax Filing Deadlines

The deadline for filing New York State income tax returns is typically April 15th, coinciding with the federal tax deadline. However, if this date falls on a weekend or holiday, the deadline may be extended to the next business day.

Requesting an Extension

Taxpayers who need additional time to file can request an extension by submitting Form IT-201. This extension grants an additional six months to file the return, but any taxes owed must still be paid by the original deadline to avoid penalties and interest.

It's important to note that extensions only apply to the filing deadline, not the payment deadline. Taxpayers should estimate their tax liability and make payments accordingly to avoid penalties.

Penalties for Late Filing

Failing to file or pay New York State income tax on time can result in significant penalties and interest charges. The state imposes penalties for both late filing and late payment, making it crucial to meet all deadlines.

Late Filing Penalties

The penalty for late filing is generally 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25%. Additionally, a minimum penalty of $100 or 100% of the tax due, whichever is less, may apply.

Late Payment Penalties

Taxpayers who fail to pay their taxes on time may face a penalty of 0.5% of the unpaid tax for each month or part of a month the payment is late, up to a maximum of 25%. Interest is also charged on the unpaid balance at the rate set by the state.

Avoiding these penalties requires careful planning and timely submission of tax returns and payments.

Business Income Tax in New York

Businesses operating in New York State are subject to various tax obligations, including corporate income tax and franchise tax. The specific taxes applicable depend on the type of business entity and its activities within the state.

Corporate Income Tax Rates

For the 2023 tax year, New York State applies a flat corporate income tax rate of 6.5% on net income. Additionally, corporations may be subject to a Metropolitan Commuter Transportation District surcharge of 1.5% on taxable income above $5 million.

Franchise Tax

Corporations must also pay a franchise tax based on their capital stock or net worth. The franchise tax rate varies depending on the corporation's size and type of business.

Businesses should consult with a tax advisor to ensure compliance with all applicable state and local tax regulations.

Tax Obligations for Non-Residents

Non-residents who earn income in New York State are required to file a state income tax return and pay taxes on that income. The tax rates for non-residents are the same as those for residents, but non-residents may not qualify for certain deductions and credits available to residents.

Types of Income Subject to Tax

- Wages earned from employment in New York

- Income from New York-based investments

- Business income generated in New York

Non-residents should carefully track their New York-source income and consult with a tax professional to ensure proper reporting and payment of taxes.

Resources for Taxpayers

New York State provides numerous resources to assist taxpayers in understanding and fulfilling their tax obligations. These resources include online tools, publications, and support from the Department of Taxation and Finance.

Online Resources

- New York State Department of Taxation and Finance website

- Taxpayer Self-Service portal for filing and managing tax accounts

- Publications and forms available for download

Support Services

Taxpayers can contact the Department of Taxation and Finance through phone, email, or in-person assistance at local offices. Additionally, free tax preparation services are available for eligible individuals through programs like VITA (Volunteer Income Tax Assistance).

Utilizing these resources can help taxpayers navigate the complexities of New York State income tax and ensure compliance with all regulations.

Conclusion and Call to Action

New York State income tax is a critical component of financial planning for residents and businesses. By understanding the tax rates, filing requirements, deductions, and credits available, taxpayers can optimize their tax situation and ensure compliance with state regulations. Staying informed about the latest tax laws and utilizing available resources is essential for successful tax management.

We encourage readers to take the following actions:

- Review your tax situation and consult with a tax professional if needed

- Utilize the resources provided by the New York State Department of Taxation and Finance

- Share this article with others who may benefit from the information

- Leave a comment or question below for further discussion

Thank you for reading this comprehensive guide on New York State income tax. We hope you found it informative and helpful in navigating your tax obligations. For more articles on financial topics, explore our website and stay updated on the latest developments in taxation and personal finance.